We show the main highlights of the grain and oilseeds estimates for the 2025/26 campaign published by USDA in March 10:

Corn

Production

- Global corn production of the 2025/26 campaign would be around 1,297/4 million tons (Mt), representing a growth of 5.4% compared to the 2024/25 cycle, whose latest estimate stands at 1,230.6 Mt.

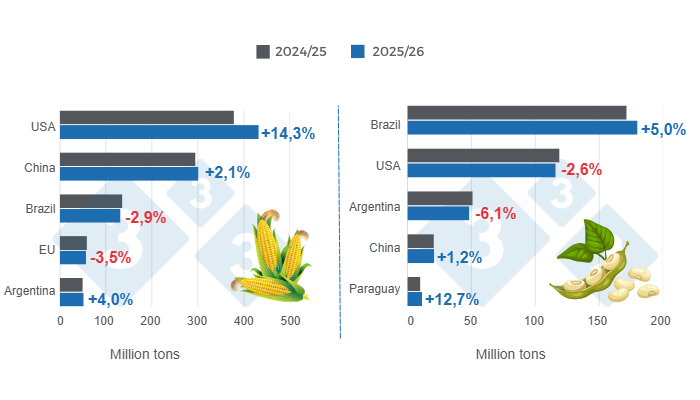

- For the US, production would reach 432,3 Mt, increasing 14.3% compared to the previous campaign (378.3 Mt), while China would increase its harvest by 2.1% to 301.2 Mt. The European Union on its side, would increase by 3.5% to 57.0 Mt, while Ukraine, with 30.7 Mt, would register an increase of 14.6% compared to the 26.8 Mt recorded in the previous cycle.

- For Brazil, production would reach 132.0 Mt, decreasing 2.9% compared to the 2024/25 campaign (136 Mt), while for Argentina, the harvest would be around 52 Mt, a figure 4.0% above the previous cycle (50.0 Mt).

Exports

- Global corn exports would increase 10.4% in this new campaign, reaching 206.8 Mt.

- The US would lead export activity with 84.8 Mt, growing 15.5% compared to the previous campaign, followed by Brazil, Argentina, and Ukraine with 43, 37 and 22 Mt, respectively.

Imports

- At the global level, corn imports would increase from 186.1 Mt in the 2024/25 campaign to 192.7 Mt in this new cycle, representing a 3.5% increase.

- Mexico would be the largest corn importer with 26.3 Mt, growing 1.4% compared to the previous campaign.

- China would increase its demand for imported corn by 338.8%, reaching 8 Mt in this new campaign, while the European Union would import 19.5 Mt, representing 4.0% increase compared to the 2024/25 cycle (18.8 Mt).

- Japan and Vietnam would import 15.5 and 13.5 Mt, respectively, representing increases of 0.3% and 12.5%.

- Colombia would increase its corn imports by 7.2%, reaching 8.0 Mt in this new cycle.

Stocks

- Ending stocks would decrease by 1.0% globally, reaching 292.7 Mt. Fr the US, stocks would increase by 37.1% while for Brazil and China would decrease by 47.5% and 6.1%, respectively.

Soybean

Production

- Global soybean production for the 2025/26 cycle would not show variations compared to the previous campaign, reaching 427.2 Mt.

- Estimates for the South American harvests indicate a 5.0% increase for Brazil, reaching 180.0 Mt, while Argentina is expected to decrease by 6.1%, reaching 48.0 Mt.

- Paraguay would increase its production by 12.7% compared to the 2024/25 (10.2 Mt), reaching a harvest of 11.5 Mt.

- For the US, production is estimated at 116.0 Mt, representing a decrease of 2.6% compared to the previous cycle (119.0 Mt).

Exports

- Global soybean exports would increase by 1.6% in this new campaign, reaching 187.2 Mt.

- Export activity would be led by Brazil with 114.0 Mt, a figure 10.5% higher than the recorded in the 2024/25 cycle, while the US would reach export volumes of 42.9 Mt, representing a decrease of 16.3% compared to the previous campaign (51.2 Mt).

- Argentina is projected to export 8.3 Mt. representing an increase of 4.8% compared to the previous (7.9 Mt).

- Paraguay would increase its exports by 20.2%, rising from 6.4 Mt in the 2024/25 campaign to 7.7 Mt in this new cycle.

Imports

- Global soybean imports would increase from 179.2 Mt in the 2024/25 to 185.6 Mt in this new campaign, representing 3.6% increase.

- China would import 112.0 Mt, a volume 3.7% higher than the previous campaign total (108.0 Mt), while the European Union would reach 14.0 Mt, representing a decrease of 4.8%.

- For Mexico, imports are expected to reach 6.7 Mt in this cycle, representing a growth of 4.1% compared to the previous campaign.

Stocks

- Ending stocks of the oilseed would increase by 1.2% globally, reaching 125.3 Mt. For the US, stock would increase by 7.6%, while for Brazil they would increase by 3.0%.

Department of Economics and Sustainability, Pig333 Latin America

USDA | USA | https://apps.fas.usda.gov/