The Spanish pig price chart in August has been flat, completely flat. As we announced in the last comment, we have surfed the crest of the wave of the maximum price in the year without distress, taking advantage of the weather slowing the growth of the pigs.

So far this year, the pig slaughterings in Spain have been 17% higher than in the same period in 2014. When writing this comment, (and during all August) the Spanish price is the European leader (with the exception of Italy, a clearly distinct importing market and insignificant in terms of exports). We are still under the apparent paradox of slaughtering as never and at the best price in comparison with all our competitors. It seems incredible but it is true.

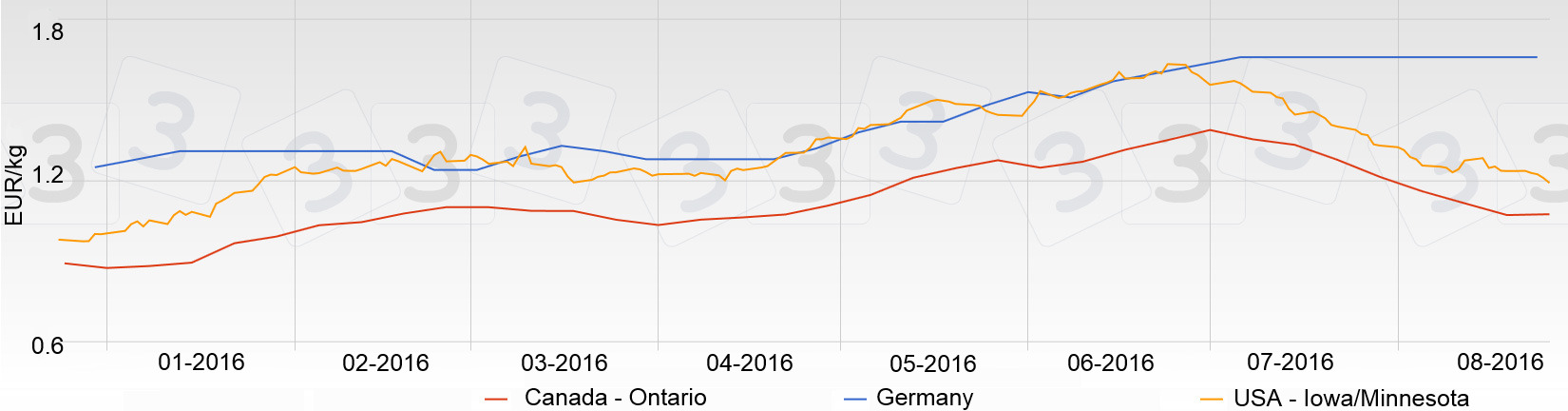

Canada and the USA reduce very quickly the price of their pigs (see the attached chart: we express the European price as the German price, because it refers to the carcass weight and it is better for comparing) and they are are standing in our way in many markets. We have no doubt at all that the European exports to third countries will suffer a lot. Europe has lost competitiveness in Asia (China and Japan), benefiting North America. This is the situation for now.

Evolution of the pig price from January to August 2016 in Germany, USA and Canada in €/kg carcass weight.

Our continental competitors (Germany, Denmark, The Netherlands and France being the most significant ones) are reducing their pig population and, as a consequence, their slaughterings. This fact will avoid the collapse that happened in autumn 2015 here and there, and it will facilitate our exports within the EU.

In our market we expect a plentiful supply of livestock. The weather and the metabolism of pigs combine (or conspire) every year in September so the pigs fatten at full speed. Also, the pigs from newly built farms will enter the slaughterings circuit. The abattoirs will have to slaughter at their maximum capacity to absorb all this supply, and we fear that if the price is not attractive for them, they will not go at full speed.

We expect September to show a bear, but not catastrophic, trend. In a months time we will be able to evaluate if the high supply is assumable by the abattoirs or if important price concessions will have to be made. The progression of the average weight of the slaughtered pigs will be a good indication.

September should show a moderate bear trend.

So far this year, the average price of a pig in our market has been €1.09/kg. Last December, January or February (being in the ditch of €0.95/kg), this average price was inconceivable, a sheer utopia, and nevertheless it has been achieved. This average price leads the prices in Europe. The increase in the pig population by 17% in two years has not been penalized up to now. So much the better.

Miguel De Cervantes Saavedra once said: "The great chances, that come unexpectedly, always bring along some suspicion."